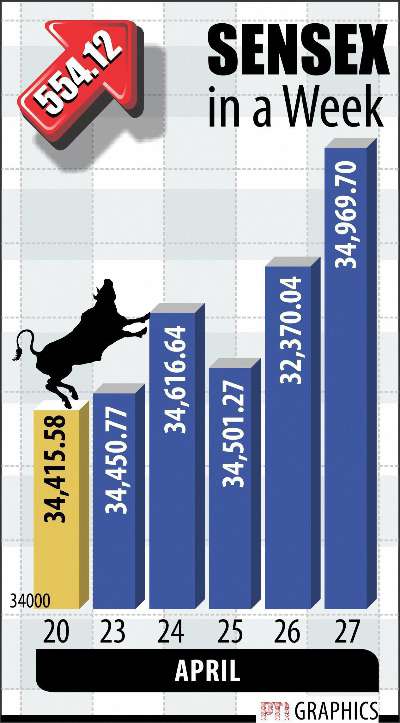

Mumbai: The benchmark Sensex accumulated gains for fifth straight week in row by a strong 554.12 points to conclude at 34,969.70, while the broader Nifty ended near the psychological 10,700-level at 10,692.30.

Bulls dominated despite the intense volatile week on visible concerns arising out of tumbling global stocks after 10-year US Treasury yield rose to four-year high of 3 per cent sapped the appetite as well as provided competition for stocks.

The domestic market further squeezed by April F&O expiry, volatile rupee dropping fresh 13-month lows along with surging global crude oil as well as sliding metal prices.

However, market drew strength mainly from encouraging corporate earnings results which met with street expectation, also normal monsoon forecast along with growth fundamentals provided strength to stock momentum as the key indices reclaimed the important 35,000-level during the week.

Strong rally in key IT stock TCS, helped the country to get another USD 100 billion company after a decade, stellar Q4 results from private lender Yes Banks brought-back investor confidence in banks and financial stocks.

Buying in key heavyweights Reliance ahead of Q4 results also build-up the gains.

The BSE Sensex started the week higher at 33,493.69 and hovered between high of 35,065.81 and low of 34,259.27 before closing the week at 34,969.70, showing a gain of 554.12 or 1.61 per cent. (The Sensex gained 1,819.04 or 5.58 per cent during previous four week session)

The Nifty also resumed the week higher at 10,592.80 and traded between 10,719.80 and 10,514.95, the index finally closed at 10,692.30, up 128.25 points, or 1.21 per cent.

In the broader market traded mixed with midcap shares gaining, while smallcap ending with losses.

Buying was led by Banks,Oil & Gas, Realty, HealthCare, Auto, IPOs, FMCG and IT sectors.

Metal, Consumer Durables, Power, PSU and Teck saw profit-booking.

Meanwhile, foreign portfolio investors (FPIs) and foreign institutional investors (FIIs) sold shares worth Rs 2,006.21 crore during the week, as per Sebi’s record including the provisional figure of April 27, 2018.

The BSE Mid-Cap index rose 118.24 points or 0.70 per cent to settle at 16,917.18. The BSE Small-Cap index rose 61.93 points or 0.34 per cent to settle at 18,239.96.

Among sectoral and industry indices, Bankex rose by

2.42 per cent, Oil & Gas 1.76 per cent, Realty 1.73 per cent, Healthcare 1.54 per cent, Auto 1.17 per cent, IPO 1.11 per cent, FMCG 0.78 per cent, Capital Gooods 0.35 per cent and IT 0.30 per cent.

However, Metal fell by 3.40 per cent, Consumer

Durables 0.71 per cent, Power 0.56 per cent, PSU 0.10 per cent and Teck 0.07 per cent.

Among the 31-share Sensex pack, 21 stocks rose and remaining 10 stocks fell during the week.

Yes Bank was the top gainer in the Sensex pack as it jumped 12.97 per cent. The bank reported 29.02 per cent rise in net profit to Rs 1179.44 crore on 27.78 per cent rise in total income to Rs 7163.95 crore in Q4 March 2018 over Q4 March 2017.

It was followed by M&M 7.61 per cent, Reliance 7.19 per cent, Axis Bank 6.40 per cent, Adani Ports 5.64 per cent, Sun Pharma 3.73 per cent, Indus Ind Bank 3.52 per cent, Bajaj Auto 2.71 per cent, Kotak bank 2.59 per cent and Asian Paints 2.50 per cent.

Wipro was the top Sensex loser last week as it lost 7.71 per cent. Its consolidated net profit fell 6.69 per cent to Rs 1,800.80 crore on 0.04 per cent rise in total income to Rs 14,304.60 crore in Q4 March 2018 over Q3 December 2017.

It was followed by Maruti 2.87 per cent, Tata Steel

2.75 per cent, NTPC 2.38 per cent, Coal India 2.23 per cent, HDFC Bank 1.94 per cent, Dr Reddy 1.09 per cent and Tata Motors DVR 1.05 per cent.

The total turnover during the week on BSE rose to Rs 16,885.82 crore as against last weekend’s level of Rs 16,335.71 crore and NSE gained to 1,73,159.52 crore compared to Rs 1,48,712.79 crore previously.

Gold extends losses

Both the precious metals lost the sheen during the week at bullion market following subdued investors offtake and slackened demand from jewellers and retailers at higher levels, also driven by weak global trend.

Traders said a weak trend overseas where a higher dollar against a basket of currencies dented safe haven appeal of gold, dampened the sentiment here.

Besides, a considerable drop in demand from jewellers and retailers at existing levels too hit the sentiment, they said.

Silver too extended losses and cracked below the Rs

40,000-mark by plunging Rs 890 to end at Rs 39,270 per kg on reduced offtake by industrial units and coin makers.

On the global front, gold prices took back some ground after a two-session skid as financial markets assessed the merits of Korea peace efforts and the first reading of first-quarter GDP, which came in slightly better than expected.

Gains for the yellow metal came even as a leading dollar measure also rose, with a pullback in the yield for the benchmark 10-year Treasury giving the commodity, which doesn’t offer a yield some ground to rise.

June gold finished USD 5.50, or 0.4 per cent, higher at USD 1,323.40 an ounce, bouncing off its lowest closing level since March 20. June gold notched a 1.1 per cent drop for the week as rising rates weighed on bullion.

Elsewhere in the metals complex, May silver lost 8.5 cents, or 0.5 per cent, to settle at USD 16.406 an ounce. July silver which is now the most-active contract, shed 7 cents, or 0.4 per cent, at USD 16.497.

For the week, the May contract for silver declined by 4.6 per cent, while the July contract fell by 4.2 per cent.

In the New York Comex trade, gold for June delivery fell to settle at USD 1,323.40 an ounce compared to last weekend’s close of USD 1,338.30, while May silver contract moved down to end at USD 16.406 an ounce from USD 17.163 earlier.

On the domestic front, standard gold (99.5 purity) resumed lower at Rs 31,260 per 10 grams from last Friday’s closing level of Rs 31,315 and hovered in a range of Rs 31,325 and Rs 31,125 before settling at Rs 31,180, revealing a loss of Rs 135, or 0.43 per cent.

Pure gold (99.9 purity) also commenced lower at Rs 31,275 per 10 grams compared to preceding weekend level of Rs 31,465 and moved in a range of Rs 31,475 and Rs 31,275 before finishing at Rs 31,330, revealing a fall of Rs 135 per 10 grams, or 0.43 per cent.

Silver ready (.999 fineness) opened higher at Rs

40,205 per kilo gram from last Friday’s closing level of Rs 40,160, later it plunged to Rs 39,210 before settling at Rs 39,270, showing a loss of Rs 890 per kilo, or 2.22 per cent.

Rupee suffers fresh blow

The rupee suffered yet another nasty blow as uneasiness roared back once again in mysterious ways driven by a crisis of confidence in the midst of deteriorating macro environment and concerns over capital outflows.

Overall, the forex market sentiment turned into dismay following panic-driven dollar buying from corporates and importers, sending the rupee tumbling down to hit multi-month lows.

Surging global curde prices and consistent widening in the trade deficit along with massive exodus of capital outflows from both equity and debt market, largely impacted the forex stability.

It was a bad week for the Indian currency – piercing through all critical support level to hit a fresh 14-month low of 66.91, before a dead-cat bounce.

India appears to be caught in a recurring economic nightmare as the rapid rise in crude prices is putting pressure on sources of macro stability -low inflation, and lower current account and fiscal deficits, a forex dealer said.

The rupee has been the worst performing Asian currency this year after strengthening over six per cent in 2017, he added.

The bond market also witnessed subdued trade with the benchmark 10-year yield curve rising further to 7.77 per cent from 7.72 per cent last weekend.

Foreign investors and funds pulled out nearly Rs 8,000 crore from the Indian capital markets so far this month due to ‘considerable’ volatility in global markets.

In the meantime, after scaling life-time high, the country’s foreign exchange reserves fell by a whopping USD 2.499 billion to USD 423.582 billion in the week to April 20, the Reserve Bank of India (RBI) said.

On the energy front, crude prices maintained their bullish ascent for the third straight week on hardening worry over Iranian sanctions amid supply concerns due to falling production in Venezuela and Angola.

Brent crude futures, an international benchmark, ended at USD 74.64 a barrel. This month, it briefly touched a high above USD 75-mark, a level last seen in late 2014.

After suffering the worst weekly loss this year, the rupee opened lower at 66.20 from last weekend level of 66.12 at the inter-bank foreign exchange (forex) market driven by intense dollar pressure.

Later it cracked all the way down to hit a fresh 14-month low of 66.91 – just below the psychological 67-mark – the level not seen since February 22, 2017.

The local unit, however managed to pull back some lost ground during the fag-end session of the week to end at 66.66, still showing a loss of 0.54 paise, or 0.82 per cent below where it was a week ago.

Scripting its third-straight weekly plunge, the rupee depreciated sharply by 169 paise against the USD.

Month to date, the rupee has lost a staggering 2.27 per cent.

The RBI, meanwhile, fixed the reference rate for the dollar at 66.7801 and for the euro at 80.7438.

On the global front, fag-end profit taking prevented the US dollar from extending its gains Friday despite stronger-than-expected first-quarter US GDP growth also supported by a combination of rising treasury yields and growing expectations for a faster pace of rate hikes.

The dollar index, which measures the greenback’s value against a basket of six major currencies shot-up to three week high of 91.31 as against 90.08 previously.

Elsewhere, the British pound remained under immense pressure after the first quarter GDP data in the UK fell short of the market expectations along with disappointing key macro releases, diminishing chances of a rate hike in near term.

The euro tumbled to fresh 3-months low against the greenback after the ECB left policy rates unchanged as expected and left the future of its asset purchasing programme unchanged.

The Bank of Japan, however kept the monetary policy unchanged as widely expected in April and abandoned the fiscal year 2019 as the time frame for reaching the 2 per cent inflation goal.

In cross-currency trade, the home currency, however staged a smart rebound against the pound sterling to finish at 91.82 from weekend’s close of 92.98 per pound and recouped against the euro to finish at 80.54 from 81.39.

The local unit also recovered against the Japanse yen to end at 60.98 per 100 yens as compared to 61.46 previously.

In the forward market, premium for dollar dropped sharply due to fresh receiving from exporters.

The benchmark six-month forward dollar premium payable for August drifted to 83.50-85.50 paise from 95-97 paise and the far-forward contract maturing in February 2019 also slumped to 212.50-214.50 paise from 225-227 paise last Friday. (PTI)

{kind=link}